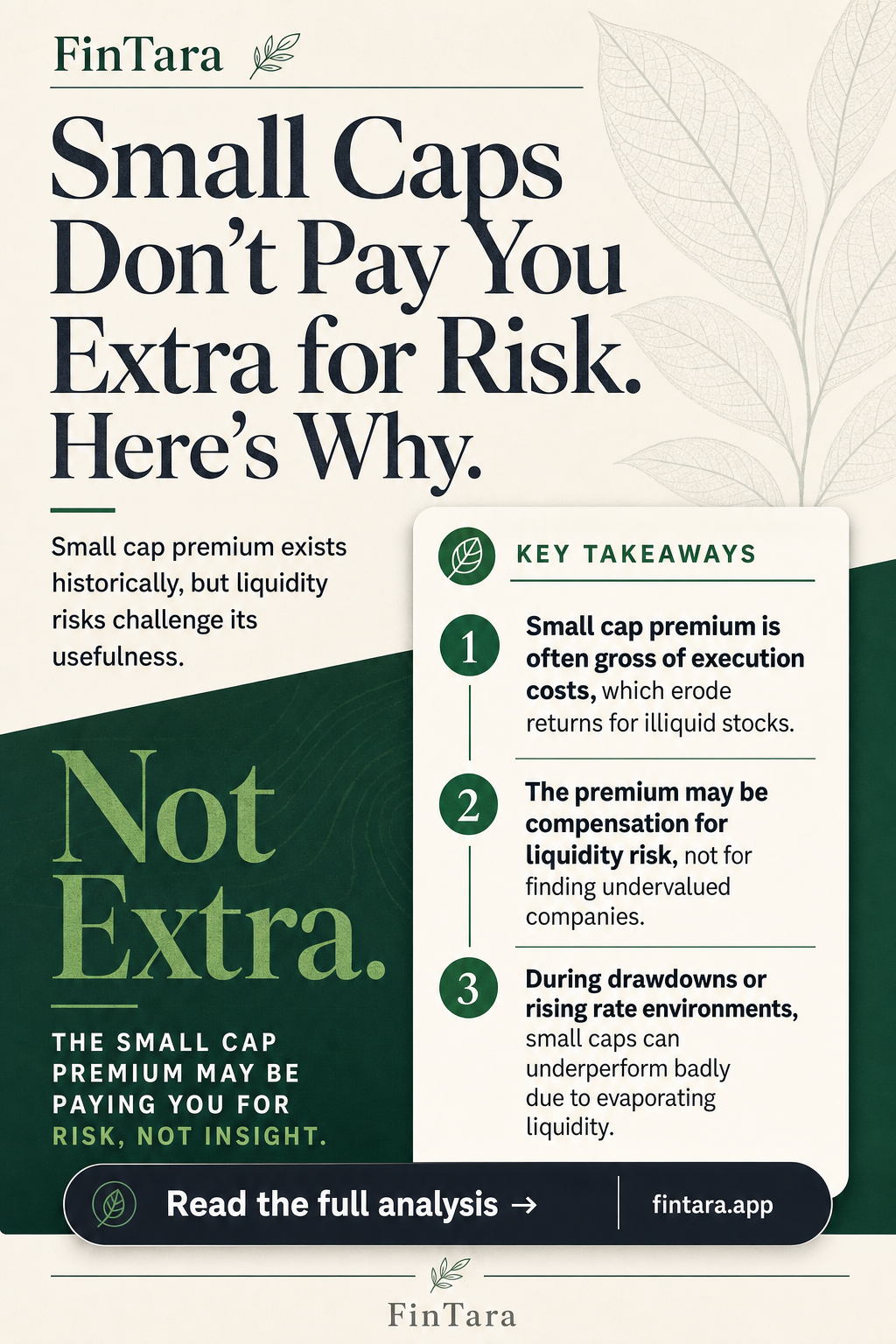

The small cap premium exists in the historical record. Whether it exists in your portfolio is a different question entirely. Most of the debate stops at "small caps outperform over time" without asking why — or whether the explanation changes what you should actually do. The liquidity argument is the most rigorous challenge to the premium's usefulness, and it deserves more scrutiny than it typically gets from retail investors chasing size-factor exposure.

What the Textbook Gets Wrong About the Premium's Source

The Fama-French three-factor model gave the small cap premium academic credibility in 1992. Size became a factor. Investors built funds around it. The logic seemed clean: small caps outperform, so tilt toward them.

The problem is that "outperform" is doing a lot of work in that sentence.

A stock that gains 12% annually but trades by appointment — wide spreads, thin order books, price impact on every meaningful-size order — does not actually deliver 12% to most investors. The published return is gross of execution costs. For small caps with limited float and low average daily volume, those costs are not rounding errors.

Illiquidity extracts its toll in several places at once. Wide bid-ask spreads cost you on entry and again on exit. Price impact — moving the market against yourself when you buy or sell — compounds that cost whenever your order is large relative to average volume. And market impact gets worse precisely when you most want out: during drawdowns, when liquidity in smaller names evaporates fastest.

This is the liquidity risk explanation in its strongest form. The "premium" isn't alpha. It's compensation for holding an asset that becomes hard to exit when sentiment shifts. You're not being rewarded for finding undervalued companies. You're being paid to accept a structural disadvantage that most institutional capital can't afford to ignore.

Retail investors often miss this because they're trading in small enough size to avoid significant price impact. But the structural argument still matters: if the premium exists because of liquidity risk, then in periods when liquidity conditions deteriorate broadly — rising rate environments, credit stress, risk-off rotations — small caps don't just underperform. They underperform badly, which is exactly when you'd least want the exposure.

The Evidence That Actually Complicates the Narrative

Liquidity risk may explain the premium, yet it rarely rewards the holder. — Photo by Tiger Lily on Pexels

Liquidity risk may explain the premium, yet it rarely rewards the holder. — Photo by Tiger Lily on Pexels

The raw historical record shows small caps beating large caps over long horizons. That's not in serious dispute. What's disputed is whether the premium survives three filters that matter to a real investor.

The first filter is transaction costs. Academic studies typically use closing prices. Real trading happens at the ask on the way in and the bid on the way out. For thinly traded small caps, that spread alone can consume a year's worth of expected premium before the calendar turns.

The second filter is survivorship bias. Small cap indices get populated by winners. Companies that went bust, got delisted, or simply stagnated drop out of the historical sample. The premium looks better than it was because the worst outcomes quietly disappear from the dataset.

The third filter is time period selection. The small cap premium in the US was concentrated in specific decades — particularly the early-to-mid periods of the historical record. More recent windows, including most of the post-2010 era, show large caps compounding well ahead of small caps for extended stretches. Investors who tilted toward small caps in 2014 waited a long time for the premium to show up.

None of this means the premium is fabricated. It means the gross number in a textbook and the net number in a brokerage account can be very different things — and the gap between them tends to widen in exactly the environments where small cap investors are already uncomfortable.

The liquidity explanation also has a secondary implication that rarely gets stated directly: if illiquidity is the source of the premium, then improving market structure should erode it over time. Electronic trading, ETF arbitrage, and broader information access have all made markets more liquid over the past two decades. If the premium has compressed since the 1990s, that's the structural reason.

When the Premium Breaks Down Hardest

Why historical outperformance doesn't guarantee future gains for small cap investors. — Photo by Jakub Zerdzicki on Pexels

Why historical outperformance doesn't guarantee future gains for small cap investors. — Photo by Jakub Zerdzicki on Pexels

Liquidity-driven premia don't fail gradually. They fail suddenly, and they fail in clusters.

The clearest failure condition is a broad risk-off environment. When institutional capital reduces equity exposure quickly, small caps bear disproportionate pressure. Large caps have deeper order books, more analyst coverage, and active options markets that provide hedging alternatives. Small caps have none of that. The exit is narrower when everyone is heading for the door.

This means small cap drawdowns tend to be deeper and longer than their large cap equivalents in the same market event. It also means the path back is slower, because the bid to buy beaten-down small caps returns before the liquidity does.

A second failure condition is concentration in low-quality small caps. Not all small caps carry liquidity risk equally. A small cap with strong free cash flow, low debt, and consistent earnings is a different animal from a small cap that trades on narrative and burns cash. Indices don't distinguish between them. A fund tracking a broad small cap index holds both, which means you get the illiquidity cost on the junk names without necessarily capturing the quality premium on the good ones.

The third failure condition is the one investors reliably underestimate: holding period mismatch. The small cap premium, to the extent it's real, materializes over long periods — think decades, not years. Most retail investors don't hold positions through multiple bear markets and full economic cycles with that kind of discipline. They trim when it hurts and add when it's already worked. The return they actually capture is well below the index return, and the index return is already gross of transaction costs.

If your actual holding behavior is 2–4 year cycles rather than multi-decade buy-and-hold, the small cap premium's historical case gets thin fast.

What a Skeptical Position in Small Caps Actually Looks Like

Cover: Office desk with small cap stock charts showing liquidity analysis — Photo by George Morina on Pexels

Cover: Office desk with small cap stock charts showing liquidity analysis — Photo by George Morina on Pexels

The skeptical case against the small cap premium doesn't require avoiding small caps entirely. It requires building the exposure differently.

The first adjustment is quality filtering. Small cap value — specifically, small cap stocks with earnings, manageable debt, and genuine free cash flow — has a more durable historical case than small cap broadly. The quality screen removes the most illiquid, narrative-driven names while keeping the size exposure. ETFs like IWD (Russell 1000 Value) don't give you small cap exposure, but funds like AVUV (Avantis US Small Cap Value) attempt to blend the size and value factors with a quality tilt. The expense ratios are higher than plain-vanilla index funds, but the construction is more deliberate.

The second adjustment is liquidity awareness at the individual stock level. When evaluating a specific small cap position, average daily volume matters more than most retail investors acknowledge. A rough rule: if your intended position size represents more than 1% of a stock's average daily volume, price impact becomes a real execution cost. For many retail-sized accounts, this constraint is less binding — but it's still worth knowing how quickly you could exit if sentiment shifted.

The third adjustment is sizing the position to match your actual conviction about the holding period. Small cap exposure that represents 5% of a portfolio held through a full market cycle is a different proposition than 20% that gets trimmed whenever drawdowns start. The premium, if real, requires patience that most investors don't actually exercise. Size the position to what you'll hold through a 35% drawdown without flinching — not what looks right when the chart is trending up.

The deeper point is this: the liquidity risk argument doesn't make the small cap premium fake. It makes it conditional. You earn it if you hold through illiquid markets, accept wider spreads, sit through deeper drawdowns, and stay patient over cycles that outlast most investors' resolve. That's a legitimate risk premium. But calling it "free outperformance from a size tilt" is a misread of what you're actually signing up for.

FAQ

Is the small cap premium still real after accounting for transaction costs?

The evidence is genuinely mixed. Gross of costs, long-run small cap outperformance appears in the historical record across multiple countries. Net of real-world spreads and price impact — especially for less-liquid names — the premium compresses significantly. For index-level small cap exposure via high-volume ETFs, costs are manageable. For individual illiquid small caps, execution costs can erase most of the theoretical edge.

Which ETFs give small cap exposure without the worst liquidity drag?

IWM (Russell 2000, ~0.19% ER, among the most liquid small cap vehicles by average daily volume) minimizes trading friction at the fund level. AVUV targets small cap value with a quality overlay. Both avoid the individual-stock liquidity problem. The underlying holdings still carry illiquidity risk in stress scenarios — that risk doesn't disappear at the ETF wrapper level, it just concentrates differently.

Does the Fama-French size factor still hold in the post-2010 data?

Large caps, led primarily by mega-cap US technology, dominated returns for most of the 2010–2023 period. The size factor delivered negative or near-zero contribution in that window. Whether that's mean reversion waiting to happen or a structural shift tied to winner-take-all platform economics remains unsettled. The historical multi-decade case for the premium doesn't automatically validate a near-term expectation.

How does rising interest rates affect small cap liquidity specifically?

Small caps carry higher proportions of floating-rate debt on average than large caps. When rates rise sharply — as they did in 2022 and into 2023 — refinancing costs hit smaller balance sheets harder and faster. That fundamental stress compounds the liquidity problem: investors reduce exposure to riskier, harder-to-exit positions at the same time the underlying business fundamentals weaken. The two pressures arrive together, not sequentially.

When does it actually make sense to avoid small cap exposure entirely?

Three specific conditions argue for reducing small cap allocation: when credit spreads are widening quickly (a signal that liquidity is tightening across risk assets), when your investment horizon is under five years, or when your portfolio already carries significant concentration in cyclical or high-beta names. Adding small cap exposure to a portfolio that already behaves like a leveraged bet on growth doesn't diversify — it doubles down.

The premium may be real. Whether you actually capture it depends on costs, discipline, and holding behavior that most investors overestimate in advance and underdeliver in practice.