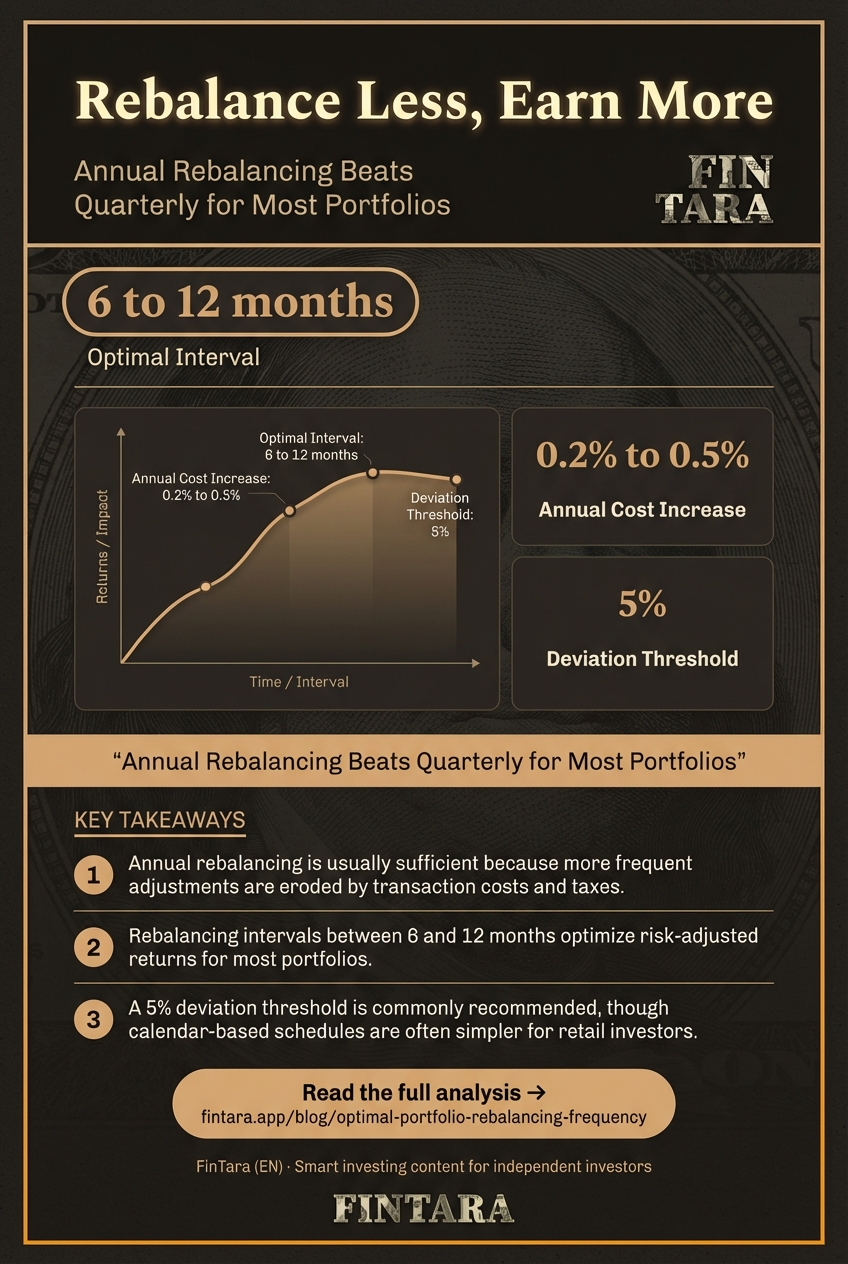

Rebalancing your portfolio once a year is usually enough. Academic research and historical data show that intervals between 6 to 12 months optimize risk-adjusted returns for most investors. Vanguard's research suggests annual rebalancing is sufficient because transaction costs and taxes eat into returns with more frequent adjustments. This matters for retail investors because every unnecessary trade costs real money. The 5% threshold bands are commonly recommended, but calendar-based annual rebalancing is simpler and effective. For taxable accounts, tax-loss harvesting can offset costs, but that requires discipline. The core insight is that less is more: you do not need to rebalance quarterly unless your portfolio drifts significantly beyond your risk tolerance.

Why Calendar-Based Rebalancing Usually Wins

Most retail investors default to calendar-based rebalancing—quarterly, semi-annually, or annually—because it's simple and predictable. The evidence shows annual rebalancing typically captures the bulk of risk control without the friction of frequent trading. Historical backtesting indicates that rebalancing intervals between 6 and 12 months yield the best risk-adjusted returns. The key is consistency: you stick to a schedule and avoid emotional reactions to market swings. Quarterly rebalancing increases transaction costs by roughly 0.2 to 0.5 percent annually, according to industry estimates. Over a decade, that compounds into meaningful drag on performance. Annual rebalancing reduces this drag while still preventing your portfolio from drifting too far from its target allocation. The inversion here is critical: when markets are calm and correlations are low, you should rebalance less frequently. Frequent rebalancing during low-volatility periods costs money without delivering material risk reduction.

Threshold Bands vs. Calendar Schedules

Hands analyzing financial graphs and charts from a folder on a desk. — Photo by Kampus Production on Pexels

Hands analyzing financial graphs and charts from a folder on a desk. — Photo by Kampus Production on Pexels

Threshold-based rebalancing triggers a trade when an asset class deviates from its target by a set percentage, commonly 5 percent. This approach is more responsive to market movements but can lead to whipsaw trades in volatile markets. Calendar-based rebalancing, by contrast, is time-based and ignores interim volatility. The trade-off is between precision and cost. Academic studies show that threshold bands work well for portfolios with high volatility assets, like emerging market stocks or small-cap funds. For a standard 60/40 stock-bond portfolio, annual calendar rebalancing often delivers similar risk control with lower costs. The inversion is this: if your portfolio includes assets with low correlation and moderate volatility, threshold bands may trigger too often and erode returns. In practice, combine both: use a 5 percent threshold for major deviations but default to an annual calendar check. Tools like Personal Capital or portfolio trackers in IBKR can automate this monitoring.

Transaction Costs and Tax Implications

Close-up of business report with colorful charts on a wooden desk. — Photo by RDNE Stock project on Pexels

Close-up of business report with colorful charts on a wooden desk. — Photo by RDNE Stock project on Pexels

Transaction costs are the silent killer of rebalancing strategies. Every trade incurs commissions, bid-ask spreads, and potential market impact. For retail investors using brokers like IBKR, costs are low but not zero. Tax implications in taxable accounts add another layer: selling winners triggers capital gains taxes. Vanguard's research notes that rebalancing can cost 0.2 to 0.5 percent annually in friction. The inversion here is crucial: if your portfolio is in a tax-advantaged account like an IRA or 401(k), rebalancing is cost-free and should be done more aggressively. In taxable accounts, use tax-loss harvesting to offset gains. For example, if you need to trim an overweight stock position, sell a losing position elsewhere to neutralize the tax bill. This requires tracking lots and understanding wash-sale rules, but tools like IBKR's tax-loss harvesting features can assist. The bottom line: prioritize tax efficiency in taxable accounts and keep rebalancing frequency low.

Asset Class Interactions and Portfolio Drift

Different asset classes rebalance differently. Stocks typically have higher volatility than bonds, so equity allocations drift faster. A 60/40 portfolio might see stocks grow to 65 percent within a year during a bull market. Bonds, with lower volatility, drift slower. This means your rebalancing frequency should account for the highest-volatility component. If you hold international stocks or emerging markets, consider more frequent checks—perhaps semi-annually—because those assets swing wider. However, the inversion is valuable: if your portfolio is dominated by low-volatility assets like bond funds or dividend stocks, annual rebalancing is more than enough. The goal is to prevent risk exposure from exceeding your intended level. Letting a portfolio drift too far increases drawdown risk during corrections. Historical data shows that a 60/40 portfolio left unbalanced for three years can drift to 70/30, raising volatility by several percentage points. Annual rebalancing keeps this drift in check without unnecessary trading.

Tools and Automation for Retail Investors

Practical implementation matters. Most retail investors lack time to manually track and rebalance. Automation is key. IBKR's portfolio analyzer lets you set allocation targets and receive alerts when drift exceeds a threshold. Personal Capital provides a free dashboard with rebalancing recommendations. For hands-off investors, target-date funds or robo-advisors like Betterment automate rebalancing entirely. However, the inversion here is instructive: automation can lead to over-trading if not calibrated correctly. Set your thresholds wisely—5 percent for major allocations, 2 percent for individual positions. Use calendar reminders as a fallback. Tax-loss harvesting tools in IBKR or via services like Wealthfront can offset rebalancing costs in taxable accounts. The key is to pick a system you can stick to. Complexity is the enemy of execution. A simple annual calendar reminder paired with a 5 percent threshold covers most scenarios.

FAQ

How often should I rebalance my portfolio?

Annual rebalancing is sufficient for most investors. Academic studies show intervals between 6 and 12 months optimize risk-adjusted returns. Use a 5 percent threshold for major deviations.

Is quarterly rebalancing better than annual?

Quarterly rebalancing increases transaction costs by 0.2 to 0.5 percent annually without meaningful risk reduction. For most portfolios, annual rebalancing delivers similar risk control at lower cost.

What are the tax implications of rebalancing?

In taxable accounts, selling winners triggers capital gains taxes. Use tax-loss harvesting to offset gains. In tax-advantaged accounts like IRAs, rebalancing is cost-free.

Should I use threshold-based or calendar-based rebalancing?

Combine both. Use a 5 percent threshold for major deviations but default to an annual calendar check. This balances responsiveness with cost control.

How do transaction costs affect rebalancing decisions?

Transaction costs erode returns, especially with frequent trading. Estimates suggest 0.2 to 0.5 percent annual drag. Keep rebalancing frequency low to minimize costs.

What is the best rebalancing strategy for retirement accounts?

In retirement accounts, tax implications are absent, so rebalancing can be more frequent. Annual or threshold-based rebalancing works well, focusing on risk control rather than tax efficiency.