Oil export bans move refining margins, regional price spreads, and shipping routes faster than most equity portfolios can react. Most coverage treats them as geopolitical noise. They're not. When a major producer restricts fuel exports — to defend domestic supply, respond to sanctions pressure, or manage a price squeeze — the effect lands in specific, traceable places: tanker utilization rates, regional crack spreads, and the equities of refiners operating downstream of the restricted flow. The portfolio impact is mechanical, not speculative.

What Most Analysts Miss When an Export Ban Hits

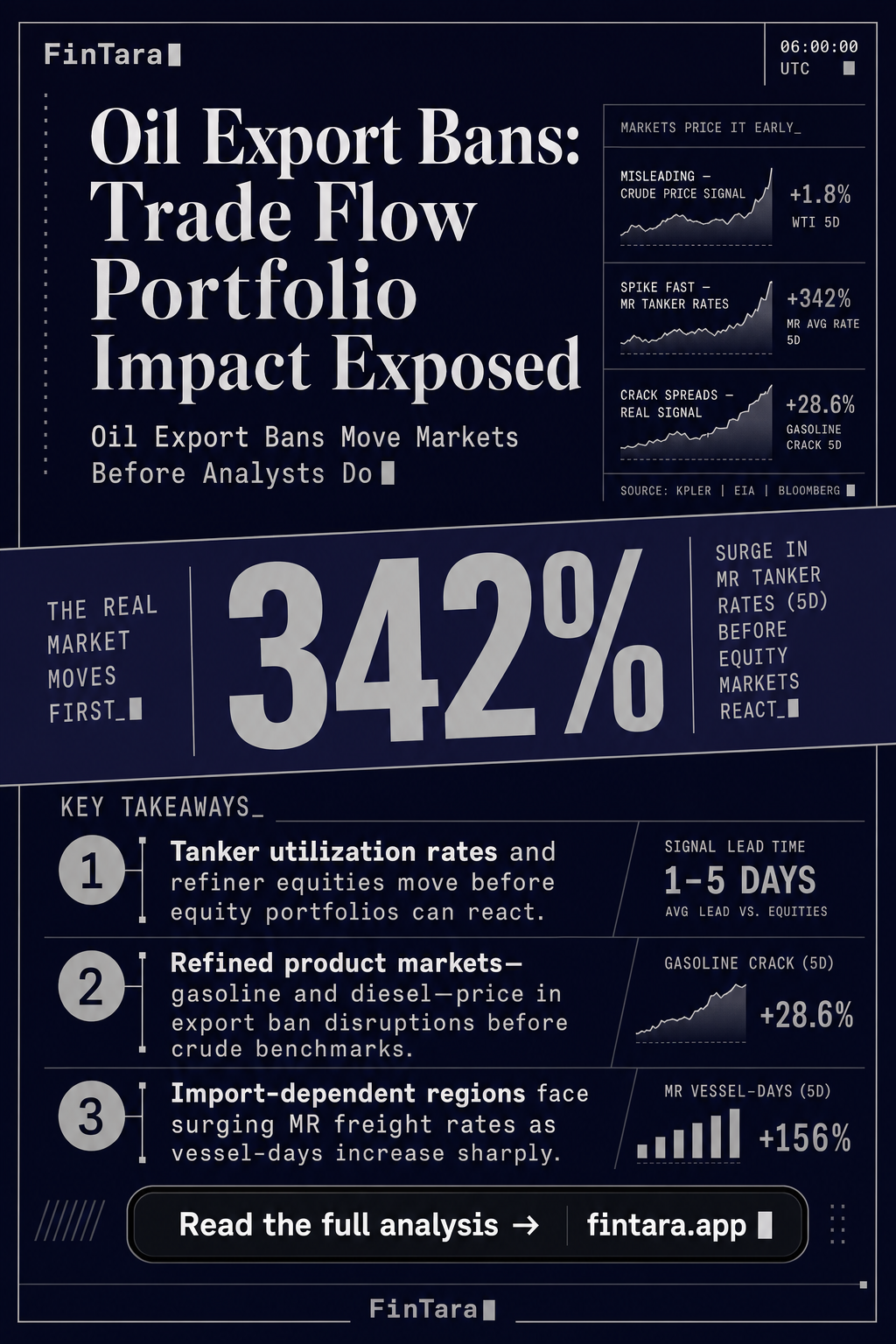

The instinct is to watch crude. That's the wrong instrument.

When a country restricts fuel exports, the crude market absorbs the headline. But the real signal lives in refined products — gasoline, diesel, jet fuel. Export restrictions reduce the supply of finished product to import-dependent regions. Those regions respond by sourcing longer, pulling product from farther afield. Longer routes mean more vessel-days. More vessel-days tighten tanker capacity. Tighter capacity pushes freight rates up.

Crude prices may barely move. Product spreads and MR tanker rates can move sharply within days.

This is not a secondary effect. It's the primary transmission mechanism. Retail investors who track only Brent or WTI during an export ban are watching the wrong line.

The refining margin — the crack spread — is where the disruption prices in. Regions that previously imported cheap product from the restricted exporter now face higher delivered costs. Their local refiners, if any, capture the margin improvement. Their fuel importers absorb the hit. Mapping which refiners sit downstream of the newly disrupted flow is more actionable than watching benchmark crude.

The Trade Flow Disruption Has a Specific Anatomy

Export bans don't create a shortage. They create a routing problem.

Global fuel supply is rarely destroyed by an export restriction. It gets redirected. The exporter holds product domestically or reroutes to friendly markets. The previously-served import region scrambles for alternative supply — drawing barrels from Europe, the US Gulf Coast, or India, depending on the product type and geography.

This rerouting increases tonne-miles. Product that used to travel a short haul now travels a long haul. The clean tanker market — MR and LR1/LR2 vessels — absorbs the demand surge first.

Consider the structure: a ban on fuel exports from a major Asian producer pushes Southeast Asian importers toward Middle Eastern or European product. The voyage lengths double or triple. A vessel that completed four round trips per quarter might now complete two. Effective fleet capacity shrinks without a single ship leaving the market.

For investors, this dynamic is readable in advance — not with certainty, but with direction. Shipping equities tied to clean product tankers respond to tonne-mile demand, not just vessel count. When an export ban extends voyage lengths, the equities of product tanker operators typically re-rate before the freight rate indices fully reflect the move. The signal leads the data.

This is exactly the mechanism that makes sanctions-driven shipping dislocations so persistent — a related dynamic covered in the context of vessel flow changes shipping sanctions and vessel flow changes 2025.

When the Export Ban Trade Breaks Down

Refining margins react to export bans before equity markets price the risk. — Photo by Tom Fisk on Pexels

Refining margins react to export bans before equity markets price the risk. — Photo by Tom Fisk on Pexels

The routing disruption thesis has a failure condition. It's worth naming precisely.

The trade breaks down when the import-dependent region has a viable domestic alternative — or when the ban is short enough that the market bridges it with inventory rather than rerouting. If a country holds large refined product stockpiles, the tonne-mile surge never materializes. Tankers don't move. Freight rates don't lift.

Duration matters enormously. A two-week export restriction creates noise. A three-month restriction reshapes route economics. Investors who position in tanker equities or downstream refiners on a short-duration ban will often see the thesis fade before it confirms.

The second failure condition is demand destruction. If the import-dependent region responds to higher delivered costs by reducing consumption rather than sourcing longer, the expected tonne-mile increase doesn't arrive. This is more common in price-sensitive emerging markets than in OECD economies.

The third failure condition is policy reversal. Export bans are administrative decisions. They can lift overnight. The 2023 Chinese fuel export restriction, which tightened Asian diesel supply and briefly lifted European crack spreads, reversed as domestic conditions shifted. Positions built on structural rerouting assumptions can unwind faster than they built.

The trade is directionally sound. It is not duration-proof. Sizing accordingly — not betting on a sustained move — is the practical discipline.

How to Read the Signal and Position Accordingly

Tanker loading crude oil as export bans alter shipping routes and portfolio exposure. — The original uploader was Snow storm in Eastern Asia at English Wikipedia., via Wikimedia Commons

Tanker loading crude oil as export bans alter shipping routes and portfolio exposure. — The original uploader was Snow storm in Eastern Asia at English Wikipedia., via Wikimedia Commons

{kind=link}

Position construction here is about instruments, not conviction.

The cleanest equity expression of a product tanker tonne-mile surge is in companies with pure-play clean tanker exposure. When an export ban extends voyage lengths, these businesses earn more per vessel-day without adding ships. The revenue lift is temporary but often meaningful within a quarter.

For refining exposure, the question is geography. A refiner that sits in an import-dependent region competing with the newly-restricted exporter captures a margin improvement. A refiner in the restricted country's home market may face the opposite — oversupply of domestic product and compressed margins. Same sector, opposite directional exposure. Getting the geography right matters more than picking the right refining name.

Macro investors sometimes express the trade through crude differentials — the WTI-Brent spread, or regional product premiums. Diamondback Energy has publicly flagged the WTI-Brent gap as a watch item in the context of US export ban concerns, noting that a US restriction would widen the spread by trapping cheaper domestic crude. That's not currently policy, but the sensitivity is already priced into the debate.

The practical framework for a retail investor:

- Identify which import-dependent region loses supply access

- Map the alternative sourcing routes and voyage distance increase

- Screen clean product tanker operators with meaningful exposure to those routes

- Set a time horizon consistent with the ban's expected duration — typically one to two quarters maximum

- Exit when either the ban lifts or freight rate data fails to confirm the tonne-mile thesis

The signal doesn't require a view on geopolitics. It requires reading trade route arithmetic. For a deeper look at how sanctions-linked shipping disruptions create persistent dislocation in vessel rates, the analysis at shipping sanctions and vessel flow changes 2025 covers the structural parallel.

One thing to track in Q2 2026: the ongoing pressure on product export volumes from several producers responding to domestic energy security concerns. Clean tanker spot rates have shown sensitivity to these flows in recent months. The data isn't conclusive yet, but the directional setup matches the pattern described above.

Buffett's February 2026 13F adds a footnote worth noting. He trimmed Occidental Petroleum and kept Chevron at 7.2% of the portfolio. That's not a trade signal — it's a reminder that energy exposure at the portfolio level is being managed actively, not treated as a passive hold. Retail investors should apply the same discipline to any energy position built on a binary geopolitical catalyst.

The edge in this trade isn't predicting which country bans what. It's reading the routing math after the ban is announced and acting before the consensus catches up.

FAQ

Does an oil export ban affect crude prices or product prices more?

Product prices typically move faster and further. Export bans restrict finished fuel — diesel, gasoline, jet fuel — not crude directly. Import-dependent regions bid up available product, widening crack spreads in the affected geography. Crude benchmark prices like Brent often absorb the headline with minimal movement while regional diesel premiums spike.

Which tanker type benefits most from extended voyage lengths caused by export bans?

Medium Range (MR) tankers carry clean refined products on shorter trade routes and benefit most when those routes elongate. LR1 and LR2 vessels capture longer-haul product movements. Crude tankers (VLCCs) are less affected — the disruption lives in the clean product market, not crude logistics.

How long does a typical export ban last before the market reroutes fully?

Historical episodes suggest three to eight weeks for rerouting to show up in freight rate indices. The 2023 Chinese diesel export restriction ran roughly two months before conditions normalized. Restrictions under six weeks are often bridged by inventory drawdowns rather than triggering full rerouting — meaning the tonne-mile surge never fully arrives.

Are US energy equities directly exposed to foreign export bans?

Exposure depends on geography. A US Gulf Coast refiner exporting diesel to Europe benefits when Asian supply is restricted and European buyers pull more US barrels. A US crude producer is less directly affected — unless the restriction tightens global product supply enough to lift crude alongside it, which historically takes four to six weeks.

How do you screen for refiners with the right geographic exposure to an export ban?

Filter for refiners whose primary export markets overlap with the newly import-constrained region. Valero and Phillips 66 both disclose export volumes by destination in quarterly filings. Cross-reference with the IEA's monthly oil trade flow data to identify which regions lost supply access. That intersection narrows the relevant names without requiring a macro view.

Does Warren Buffett's energy positioning tell retail investors anything about export ban risk?

Indirectly. His February 2026 13F shows Chevron at 7.2% of Berkshire's portfolio while Occidental was trimmed — a shift toward integrated majors and away from pure-play US producers. Integrated majors have global refining and trading operations that can reposition around export disruptions. Pure-play upstream names carry more concentrated exposure to any single trade flow shock.