Diversification alone won't protect you when every asset class moves together during a crisis. The 2008 financial collapse saw the average equity portfolio lose over 50% despite typical diversification across sectors. What actually works is a systematic approach that combines strategic asset allocation, behavioral discipline, and real-time monitoring tools. This matters because retail investors face institutional-grade volatility without institutional-grade risk frameworks. I'm outlining a multi-layered risk management system that addresses the gap between theoretical diversification and practical portfolio protection.

Why Traditional Diversification Fails in Practice

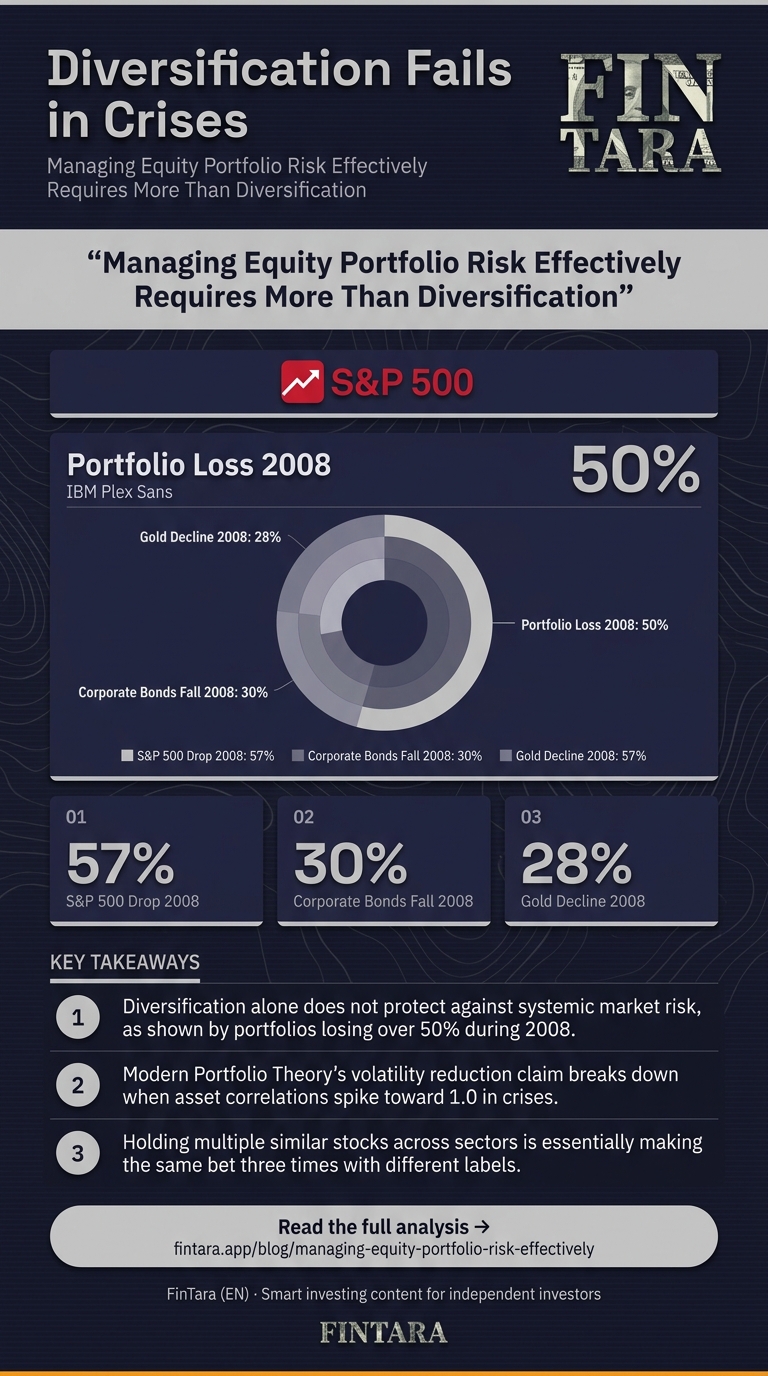

Modern Portfolio Theory claims diversification can reduce portfolio volatility by up to 30%, but this assumes assets move independently. During market stress, correlations spike toward 1.0 — meaning everything falls together. The 2008 crisis proved this: the S&P 500 dropped 57%, corporate bonds fell 30%, and even gold declined 28% in the initial panic. Your "diversified" portfolio wasn't diversified when it mattered most.

The problem isn't diversification itself — it's the assumption that holding different assets equals protection. True risk management requires understanding which risks diversification actually addresses (idiosyncratic company risk) and which it doesn't (systematic market risk). When every stock in your portfolio responds to the same macro shock, sector allocation becomes meaningless.

This is where most retail investors stumble. They build portfolios with 20+ holdings across sectors, believing they've achieved safety. But if you're holding large-cap tech, mid-cap growth, and small-cap momentum stocks, you've essentially made the same bet three times with different labels.

Behavioral Risk Management: Your Biggest Vulnerability

A trader examines cryptocurrency data, representing how modern portfolios face correlated risks during crises that challenge traditional diversification. — Photo by Tima Miroshnichenko on Pexels

A trader examines cryptocurrency data, representing how modern portfolios face correlated risks during crises that challenge traditional diversification. — Photo by Tima Miroshnichenko on Pexels

The most dangerous risk in your portfolio isn't market volatility — it's your own decision-making under pressure. Institutional investors lose 2-3% annually to behavioral biases, according to research from Dalbar. For retail investors, the number is closer to 5-7%. The gap comes from selling at market bottoms and buying at peaks, driven by fear and FOMO rather than data.

Risk management starts with acknowledging that you will panic. The 2020 COVID crash saw retail investors net sell $38 billion in March, missing the 68% recovery that followed by December. Your risk framework must account for this predictable irrationality.

The solution isn't willpower — it's structure. Set pre-defined rules for when you'll rebalance, when you'll hedge, and when you'll reduce exposure. These rules must be written down and automated where possible. If your plan says "reduce equity exposure by 20% when the VIX crosses 30," you execute that rule regardless of what CNBC is saying that morning.

This is also why I don't recommend individual stock picking for risk-managed portfolios unless you have the time and discipline to monitor positions daily. The emotional weight of watching a single position drop 40% destroys rational decision-making for most people.

Real-Time Risk Monitoring Tools and Metrics

A stock trader intensely studies data across screens, highlighting the depth of analysis required to manage equity portfolio risk effectively. — Photo by Jakub Zerdzicki on Pexels

A stock trader intensely studies data across screens, highlighting the depth of analysis required to manage equity portfolio risk effectively. — Photo by Jakub Zerdzicki on Pexels

You can't manage what you don't measure. Value at Risk (VaR) models are used by 70% of institutional investors, but retail investors typically lack access to these tools. The good news: several accessible platforms now offer institutional-grade risk analytics at retail prices.

Portfolio Visualizer provides free Monte Carlo simulations that show your portfolio's potential drawdowns across thousands of market scenarios. Run a 10,000-iteration simulation with your current holdings, and you'll see the 95% confidence interval for maximum drawdown. If that number scares you, your allocation is too aggressive.

For daily monitoring, I use a combination of correlation matrices and stress testing. Tools like Finviz's correlation heat map reveal which holdings move together — if your top 5 positions show correlation above 0.8, you don't have diversification, you have concentration in a single factor. The key metric to watch is your portfolio's beta to the S&P 500. If you're running above 1.1, you're amplifying market moves rather than dampening them.

Another critical metric is your maximum drawdown history. Track this monthly: what's the worst peak-to-trough decline your portfolio has experienced? If it's exceeded 25% in the past year, your risk tolerance and allocation are misaligned. The goal isn't zero drawdown — it's ensuring you can stomach the decline without selling at the bottom.

When Risk Management Strategies Break Down

Professional reviewing equity portfolio risk charts at office desk — Wikipedia contributors, via Wikimedia Commons

Professional reviewing equity portfolio risk charts at office desk — Wikipedia contributors, via Wikimedia Commons

Every risk framework has failure conditions, and recognizing them prevents false confidence. The 2008 crisis exposed that standard VaR models break down when market liquidity vanishes. VaR measures typical volatility but doesn't account for tail events where correlations spike and bid-ask spreads explode.

Stress testing your portfolio against historical crises reveals these gaps. Run your holdings through the 2008 scenario, the 2000 dot-com crash, and the 2020 COVID drop. If your portfolio would lose more than 40% in any of these, your risk controls are insufficient for the next crisis — because the next crisis won't be identical, but it will rhyme.

Hedging strategies also fail when executed poorly. Protective puts can limit downside to 10-15%, but only if you size them correctly and roll them consistently. Most retail investors buy puts after the market has already dropped, paying premium prices when insurance is most expensive. The correct approach is to buy protection during calm periods, when VIX is low and options are cheap.

Behavioral breakdown is another failure point. Your risk rules only work if you follow them. The 2022 bear market tested every investor's discipline — those who sold in June missed the July-August rally that recovered 50% of losses. Your framework must include accountability measures: a written investment policy statement, a trusted third party to review decisions, or automated rules that remove emotion from execution.

What to Actually Do: A Step-by-Step Risk Framework

Start with your investment policy statement. Write down your target asset allocation, maximum acceptable drawdown, and rebalancing rules. This document should be specific enough that someone else could execute it without your input. Include triggers like: "Reduce equity exposure by 10% when the 10-year Treasury yield rises above 4.5%."

Next, implement position sizing rules. No single position should exceed 5% of your portfolio value, and no sector should exceed 20%. This isn't about diversification for its own sake — it's about preventing one bad decision from destroying your returns. If you're concentrated in tech and tech crashes, you're forced to sell at the bottom to meet living expenses.

For hedging, consider a layered approach. Use broad market puts on SPY or QQQ for systemic protection, sized at 1-2% of portfolio value annually. This costs you 1-2% in good years but caps your downside during crashes. For individual positions, use trailing stop-loss orders at 15-20% below purchase price. These aren't perfect — gaps can blow through stops — but they enforce discipline when emotions run high.

Finally, schedule quarterly risk reviews. In each review, run your portfolio through the stress tests, check correlation matrices, and verify your allocation matches your policy statement. If you've drifted more than 5% from target, rebalance immediately. This discipline of regular review prevents the slow accumulation of risk that happens when you ignore your portfolio for months.

FAQ

What are the best strategies to manage risk in an equity portfolio?

The best strategies combine three layers: strategic asset allocation based on your risk tolerance, behavioral rules that prevent emotional decisions, and real-time monitoring using tools like Portfolio Visualizer and correlation matrices. Diversification alone is insufficient — you need structure and discipline.

How often should I rebalance my equity portfolio to manage risk?

Quarterly rebalancing balances transaction costs with risk control. Set tolerance bands of ±5% from your target allocation — if any holding drifts beyond that, rebalance immediately. More frequent rebalancing increases costs; less frequent lets risk accumulate unchecked.

What tools can I use to measure portfolio risk?

Use Portfolio Visualizer for Monte Carlo simulations and drawdown analysis, Finviz for correlation heat maps, and your brokerage platform's risk analytics (most now offer beta and sector exposure). Track your maximum drawdown monthly and your portfolio beta relative to S&P 500.

How does diversification reduce risk in equity investments?

Diversification reduces idiosyncratic risk — company-specific events — but doesn't protect against systematic market risk. During crises, correlations spike and diversification fails. True risk reduction requires pairing diversification with hedging and behavioral discipline.

Can hedging with options protect my portfolio from market crashes?

Protective puts can limit downside to 10-15%, but only if sized correctly (1-2% of portfolio annually) and purchased during calm periods. Most investors buy puts after crashes, paying premium prices. Hedging works when it's insurance, not a panic reaction.

What is Value at Risk (VaR) and how is it calculated for equities?

VaR estimates the maximum expected loss over a given period at a certain confidence level. For equities, it's typically calculated using historical simulation or Monte Carlo methods. Retail investors can use Portfolio Visualizer's free tools to approximate VaR, but remember — VaR breaks down during tail events and should never be your only risk measure.