A 0.03% expense ratio on a $10,000 investment costs you just $3 annually. That same investment in a 1.00% fund costs $100 every year. Over 30 years, that fee difference compounds into tens of thousands in lost returns. This is why low-cost ETFs are foundational for retail portfolios. But the headline expense ratio is only half the story. The real cost drag comes from bid-ask spreads and tax inefficiencies that most articles ignore. If you're building a portfolio with limited capital, you need to understand these hidden mechanics before you buy.

The Expense Ratio Illusion

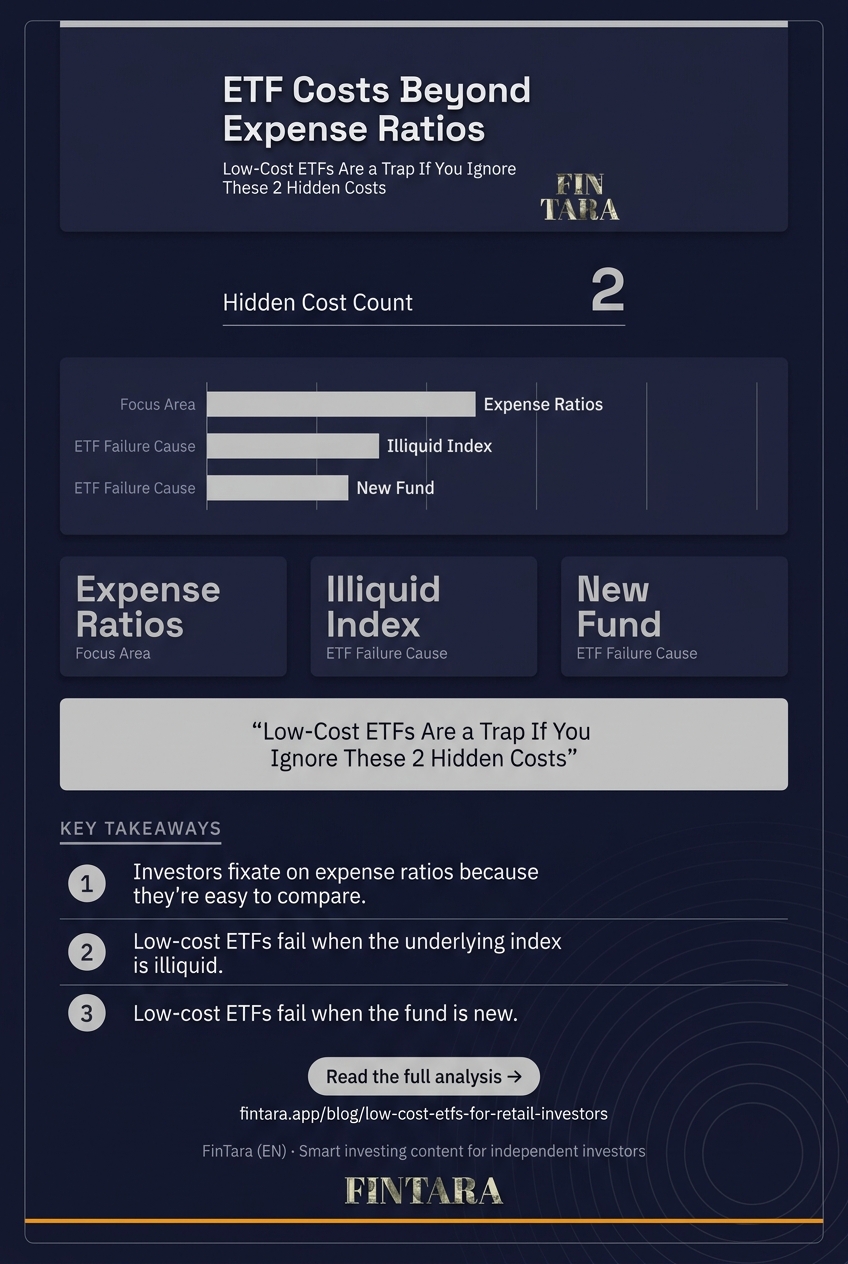

Investors fixate on expense ratios because they're easy to compare. Vanguard S&P 500 ETF (VOO) charges 0.03%. iShares Core S&P 500 ETF (IVV) also charges 0.03%. Schwab US Broad Market ETF (SCHB) matches that 0.03% fee. On a $10,000 position, each costs $3 per year. The math is simple, and the savings are real. A 1.00% fee would cost $100 annually. Over decades, that gap widens into a massive performance drag. But focusing solely on expense ratios creates blind spots.

The 0.03% figure is a marketing anchor. It signals cost-consciousness, but it doesn't capture total ownership cost. Investors trading small increments monthly face a different cost structure than someone deploying a lump sum. The ETF structure itself introduces other fees that don't appear in the expense ratio. Recognizing this is the first step to avoiding a false sense of security.

Bid-Ask Spread Costs: The Hidden Drain

serious young investor analyzing stock market charts on laptop at modern office desk — Photo by AlphaTradeZone on Pexels

serious young investor analyzing stock market charts on laptop at modern office desk — Photo by AlphaTradeZone on Pexels

Every ETF trade has a spread — the gap between the buy price and the sell price. For high-volume ETFs like VOO or IVV, spreads are tight, often under $0.01 on a $500 share. But for niche or lower-volume funds, spreads can exceed $0.10 or more. If you buy $500 worth of an ETF with a $0.10 spread, you pay $0.10 immediately on entry. That's a 0.02% hidden cost on a $500 trade. On a $50 trade, it's 0.20%.

Dollar-cost averaging monthly with small increments magnifies this. Buying $100 of an ETF with a wide spread repeatedly compounds the drag. The expense ratio stays 0.03%, but the spread cost can be five to ten times higher for micro-investors. This isn't a flaw in the ETF — it's a function of market structure. High-frequency traders and market makers profit from these spreads, and retail investors eating them monthly see returns erode.

You can minimize this by using limit orders instead of market orders. Setting a limit at the mid-price between bid and ask prevents overpaying. Most brokers display the spread in real-time. If the spread exceeds 0.05% of the trade value, consider waiting or using a different ETF with tighter liquidity. For broad market ETFs, spreads are rarely an issue. For thematic or emerging market funds, they're a significant hidden cost.

Tax Efficiency: The ETF Advantage

A businessman studies stock market data on a screen, highlighting the analysis needed to avoid low-cost ETF traps. — Photo by Tima Miroshnichenko on Pexels

A businessman studies stock market data on a screen, highlighting the analysis needed to avoid low-cost ETF traps. — Photo by Tima Miroshnichenko on Pexels

ETFs use an in-kind creation and redemption process. When an investor sells shares, the ETF provider exchanges the underlying securities directly with authorized participants. No cash changes hands internally. This structure minimizes capital gains distributions. Mutual funds, by contrast, often sell securities for cash to meet redemptions, triggering taxable events for all shareholders.

In a taxable account, this matters. A mutual fund might distribute capital gains annually, creating a tax bill even if you didn't sell shares. An ETF typically avoids this. The Vanguard Total Stock Market ETF (VTI) has an expense ratio of 0.03% and rarely distributes capital gains. A comparable mutual fund might have a 0.04% expense ratio but distribute 1-2% in gains annually. The tax drag can outweigh the fee difference.

The Fidelity ZERO Total Market Index Fund (FZROX) has a 0.00% expense ratio. It's a mutual fund, not an ETF. It's also a proprietary Fidelity index, meaning you can't hold it outside Fidelity. For taxable accounts, the lack of capital gains distributions in ETFs like VTI or SCHB often provides a net benefit over a 0.00% mutual fund that triggers annual tax events. The structure matters as much as the fee.

Brokerage Platform Costs: Trading Fees and Commissions

![]() Retail investors research low-cost ETF expense ratios on their laptops — Wikipedia contributors, via Wikimedia Commons

Retail investors research low-cost ETF expense ratios on their laptops — Wikipedia contributors, via Wikimedia Commons

Most major brokers now offer commission-free trading on ETFs. Schwab, Fidelity, and Interactive Brokers (IBKR) allow you to buy and sell ETFs without transaction fees. This removes a obvious cost layer. But platforms differ in other ways. IBKR, for example, charges interest on margin balances at 5.33% for the first $100K. Schwab charges 12.325%. If you're using margin to fund ETF purchases, the interest cost dwarfs the expense ratio difference.

Fractional share availability also affects cost. Not all brokers allow fractional ETF trades. If you're dollar-cost averaging with $50 monthly, you need fractional shares to deploy capital fully. Schwab allows fractional ETF trades for S&P 500 ETFs like SCHB. Fidelity allows fractional ETF trades across most ETFs. IBKR offers fractional shares but with some limitations. If your broker doesn't support fractional ETF trades, you may hold cash drag — uninvested dollars that earn nothing.

Automatic investment plans differ too. Some brokers let you set recurring buys for ETFs without manual intervention. Others require you to place trades each month. Automation reduces behavioral risk but also hides transaction details. If your platform doesn't show the spread or allows market orders by default, you might overpay without realizing it. Check your broker's order routing and execution quality reports.

When Low-Cost ETFs Break Down

Low-cost ETFs fail when the underlying index is illiquid or the fund is new. A thematic ETF with 0.03% expense ratio and $50 million in assets might have wide spreads and poor tracking. The first ETF, SPDR S&P 500 ETF Trust (SPY), launched in 1993. It has deep liquidity and tight spreads. A newer clean energy ETF might have similar fees but trade with a 0.50% spread. The expense ratio doesn't reflect this.

Tax efficiency also breaks in certain scenarios. If an ETF tracks a niche index with high turnover, it may distribute capital gains despite the in-kind process. Active ETFs, even low-cost ones, face higher turnover and potential distributions. If you're in a high tax bracket, a 0.03% expense ratio ETF with frequent distributions could cost more than a 0.10% ETF with minimal distributions.

Dollar-cost averaging with small amounts exposes another failure point. If your broker doesn't support fractional ETF trades, you accumulate cash. If the ETF has a high minimum purchase (some mutual funds have $1,000 minimums), you can't deploy capital efficiently. Low-cost ETFs solve the fee problem but introduce liquidity and access constraints that matter for retail investors with limited capital.

What to Actually Do: Build a Cost-Efficient ETF Portfolio

Start with a broad market ETF as your core. Vanguard S&P 500 ETF (VOO) or iShares Core S&P 500 ETF (IVV) both charge 0.03%. Use a limit order to minimize spread costs. Set your limit at the mid-price between bid and ask. For liquid ETFs, the spread is negligible, but this habit protects you in less liquid funds.

Choose a brokerage that supports fractional ETF trades and automatic investing. Schwab, Fidelity, and Interactive Brokers all offer these features. Verify that your broker allows automatic recurring buys for the ETFs you select. If you're investing taxable dollars, prefer ETFs over mutual funds for tax efficiency, even if the mutual fund has a lower expense ratio.

Monitor total cost of ownership quarterly. Calculate your effective cost: expense ratio plus estimated spread cost plus any tax distributions. If the total exceeds 0.10% for a broad market ETF, reconsider your platform or trading method. For most retail investors, a two-ETF portfolio — one U.S. broad market ETF and one international broad market ETF — with 0.03% expense ratios and fractional trading access delivers the lowest feasible cost structure.

FAQ

What is the lowest possible expense ratio for an ETF?

As of 2024, several U.S. broad market ETFs charge 0.03%, including VOO and IVV. Some thematic or regional funds may charge slightly more. The lowest expense ratios are typically for large, liquid index funds tracking major benchmarks like the S&P 500 or total market.

Are low-cost ETFs safe for beginners?

Yes, if they track broad, diversified indexes. A 0.03% S&P 500 ETF is safer than a 0.03% niche thematic fund. Safety depends on diversification and liquidity, not just the expense ratio. Beginners should avoid narrow, illiquid ETFs even if fees are low.

Is it better to buy an ETF with a 0.00% expense ratio or pay a small fee?

There is no ETF with a 0.00% expense ratio. Fidelity ZERO funds are mutual funds, not ETFs. For taxable accounts, a 0.03% ETF often beats a 0.00% mutual fund due to tax efficiency. The structure matters as much as the fee.

Do I need a lot of money to invest in low-cost ETFs?

No. Many brokers offer fractional ETF trades, allowing investments as low as $1. However, wide bid-ask spreads on small trades can erode returns. Focus on high-liquidity ETFs and use limit orders to minimize hidden costs.

What is the difference between an ETF and an index fund regarding fees?

Both can track the same index, but ETFs trade intraday on exchanges while index funds price once daily. ETFs typically have lower expense ratios and better tax efficiency in taxable accounts. Index funds may offer lower minimum investments but often lack intraday liquidity.

How do I buy low-cost ETFs without paying trading fees?

Use a commission-free brokerage like Schwab, Fidelity, or Interactive Brokers. Place limit orders to avoid wide spreads. Set up automatic recurring investments if available. Avoid market orders during volatile periods to prevent overpaying.