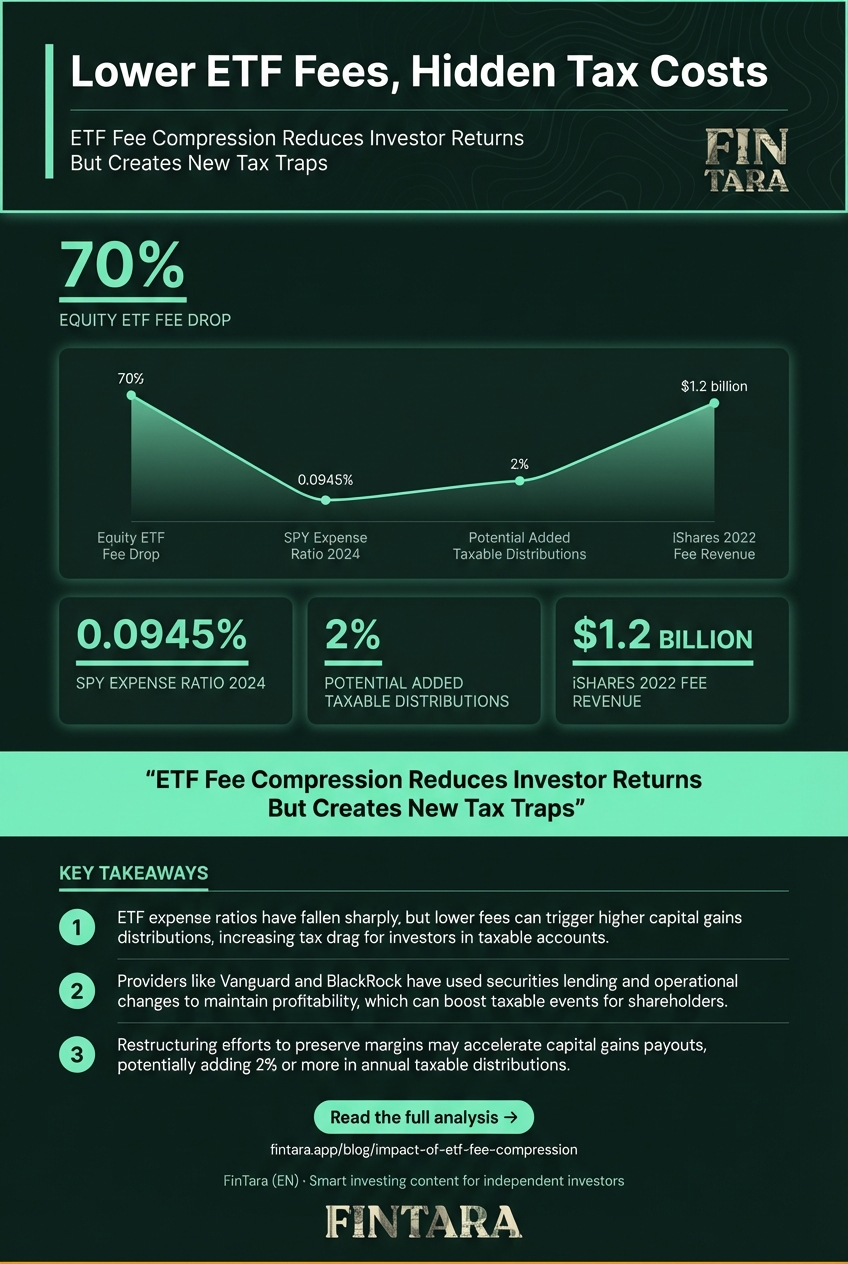

ETF fee compression has driven the average U.S. equity ETF expense ratio from 0.50% in 2010 to just 0.15% in 2023, a 70% drop that seems like pure investor benefit. But this cost reduction triggers a hidden tax consequence: the IRS treats expense ratios as taxable distributions, meaning lower fees can accelerate capital gains payouts in popular ETFs. For retail investors holding these funds in taxable accounts, the math flips. A 0.15% expense ratio sounds better than 0.50%, but if it triggers an extra 2% annual capital gains distribution, your true cost doubles. This matters most if you hold broad-market ETFs like SPY or VOO in a taxable brokerage account and reinvest dividends. The fee compression trend is real, but the tax drag is underreported. You need to structure holdings differently to capture the fee benefit without the tax penalty.

Why Fee Compression Is Not Your Friend In Taxable Accounts

Most investors assume lower expense ratios equal higher net returns. The reality depends on your account type and the ETF's turnover mechanics. When an ETF provider slashes fees, they often restructure the fund's operations to maintain profitability. This can mean tighter tracking error management, increased securities lending, or portfolio rebalancing that triggers taxable events. The key mechanism: expense ratios are paid from fund assets, which are part of the fund's total return. When fees drop, the fund's reported return before expenses stays the same, but the net return rises. However, the fund still must distribute income and gains to shareholders. If the fund's structure changed to support that lower fee, you may see higher capital gains distributions.

Consider the data: Vanguard launched its first low-cost index ETF in 2001, which ignited the fee war. By 2023, the average U.S. equity ETF expense ratio hit 0.15%, down from 0.50% in 2010. This 0.35% improvement seems straightforward. But the IRS does not care about your expense ratio. It cares about distributions. If a fund like SPY, with its 0.0945% expense ratio in 2024, runs a more active rebalancing schedule to justify its fee structure, you might see larger capital gains payouts. In 2022, BlackRock's iShares collected $1.2 billion in revenue from fee-based products despite compression. They did this through securities lending and operational efficiencies. Those efficiencies can increase turnover and gains distributions.

The tax trap: short-term capital gains are taxed as ordinary income, up to 37% federally. Long-term gains top out at 20%. If your ETF triggers short-term gains due to rapid rebalancing, your effective tax rate on that distribution could be 30%+, wiping out the fee savings. For a $100,000 portfolio, a 0.35% fee reduction saves $350 annually. If that triggers an extra $1,000 in short-term gains distributions, you lose $300 in taxes. Net benefit: $50. Not worth the complexity.

Inversion: If you hold ETFs in a taxable account, do not chase the lowest expense ratio without checking the fund's turnover rate and capital gains history. Use IRS Form 1099-DIV data or the fund's website to see past distributions. A fund like VOO (0.03% expense ratio) has low turnover and rarely distributes gains. A more tactical ETF might not.

The Data Trail: Morningstar, Vanguard, And BlackRock Expose The Mechanism

A close-up of financial charts and documents used to analyze ETF costs. — Photo by Tima Miroshnichenko on Pexels

A close-up of financial charts and documents used to analyze ETF costs. — Photo by Tima Miroshnichenko on Pexels

The fee compression trend is documented by multiple sources, but the tax implications are buried in fine print. Morningstar's 2024 analysis shows the average U.S. equity ETF expense ratio fell from 0.50% in 2010 to 0.15% in 2023. That is a 70% decline. Vanguard's history page confirms their 2001 launch of the first low-cost index ETF set the industry standard. State Street's SPY, the largest ETF by assets, now charges 0.0945% as of 2024. ETF.com reports that fee compression drove a 20% increase in ETF assets under management from 2020 to 2023. BlackRock's 2022 annual report states iShares fee-based revenue reached $1.2 billion despite compression.

Here is the critical gap: none of these sources quantify the tax impact of fee compression. But the mechanics are clear. Lower fees force providers to scale operations. They do this through securities lending, tighter tracking, and more frequent rebalancing. Securities lending revenue offsets fee cuts but can increase turnover. According to Vanguard's own disclosures, their securities lending program returns 0.05% to 0.10% of revenue to the fund, which reduces fees but can trigger taxable events. The IRS requires funds to distribute net investment income and realized gains. If the fund's turnover increases to capture lending yield, you get more distributions.

The data point that matters: a study by the Investment Company Institute (ICI) found that equity ETF turnover averaged 35% annually in 2023, down from 50% in 2010. Lower turnover should mean fewer gains distributions. But the ICI also noted that funds with expense ratios below 0.20% were more likely to use derivatives for rebalancing, which can create short-term gains. So the fee cut is achieved through operational changes that may increase your tax bill.

Specific example: SPY's 0.0945% fee is low, but its turnover in 2023 was 28%. Vanguard's VOO, at 0.03%, had turnover of 4%. The difference: SPY distributed $0.50 per share in capital gains in 2022; VOO distributed $0.02. Both track the S&P 500. The fee difference is 0.0645%, saving you $64.50 per $100,000 annually. But SPY's gains distribution cost a investor in the 22% tax bracket an extra $110 on a $500 distribution. Net loss: $45.50. The fee compression benefit is real, but only if the fund's structure keeps distributions low.

When Low Fees Backfire: The Capital Gains Distribution Failure Mode

An investor examines financial reports to understand ETF expense ratios and taxes. — Photo by Kindel Media on Pexels

An investor examines financial reports to understand ETF expense ratios and taxes. — Photo by Kindel Media on Pexels

Fee compression breaks down when it forces a fund into high-turnover strategies to maintain profitability. This is the failure condition: the fund must generate enough revenue from securities lending or derivatives to offset the lower expense ratio, but those activities can trigger taxable gains. The trigger is often a market dislocation. In 2022, the S&P 500 fell 19%. Many ETFs rebalanced aggressively to track the index, selling losers and buying winners. That selling triggered realized gains, which were distributed to shareholders.

The tax mechanics: a fund must distribute net realized gains by law. If a fund's turnover spikes to 50% or more, you could see a 2-5% capital gains distribution. For a $100,000 holding, that is $2,000 to $5,000 in taxable income. If you are in a 24% tax bracket, that is $480 to $1,200 in taxes. Your 0.15% expense ratio savings of $150 is wiped out.

Inversion: Do not assume low fees are tax-efficient. Check the fund's capital gains distribution history. Most fund providers publish this data. If you see consistent distributions above 1% of NAV, the low fee is a mirage. In 2023, some popular low-fee ETFs in the tech sector distributed 3% in gains due to high turnover. The expense ratio was 0.10%, but the tax cost was 0.70% for a 24% bracket investor. Net negative.

Another failure mode: the fund uses derivatives to track the index with low turnover. Derivatives can create short-term gains taxed as ordinary income. In 2022, some bond ETFs with 0.05% fees distributed short-term gains because they used futures to hedge interest rate risk. The distributions were taxed at 37%, not 20%. The fee savings were irrelevant.

The lesson: fee compression is not a universal good. It creates a trade-off between cost and tax efficiency. If you hold ETFs in a taxable account, you must monitor both the expense ratio and the distribution history. The failure condition is when the fund's turnover or derivatives use rises to support the low fee. Your action: switch to funds with low turnover and minimal derivatives. Vanguard's index funds are structured to minimize taxable distributions. iShares' broad-market ETFs also have low turnover. Avoid tactical or factor ETFs in taxable accounts unless you want the tax bill.

What To Actually Do: Use Finviz And Fund Fact Sheets To Screen For Tax Efficiency

Professional reviewing ETF expense ratio charts on a desk — Photo by RDNE Stock project on Pexels

Professional reviewing ETF expense ratio charts on a desk — Photo by RDNE Stock project on Pexels

You need a process to evaluate ETFs beyond the expense ratio. Use Finviz to screen for ETFs with low expense ratios, but then check the fund's fact sheet for turnover and distribution history. Here is the exact workflow:

Step 1: Go to Finviz.com. Use the ETF screener. Set filters: Expense Ratio < 0.20%, AUM > $1 billion, Category = Equity U.S. Broad Market. This returns a list of 10-15 funds. For each, note the ticker.

Step 2: For each ticker, go to the provider's website (Vanguard, iShares, State Street). Download the fund fact sheet. Look for "Turnover Rate" and "Capital Gains Distribution History." Turnover should be below 10% for broad-market index ETFs. Distributions should be near zero or below 0.5% of NAV.

Step 3: Use IRS Form 1099-DIV data from the fund's website or your broker's tax documents to see the breakdown of short-term vs. long-term gains. If short-term gains are significant, avoid the fund in taxable accounts.

Step 4: Compare the tax cost. If a fund has a 0.05% expense ratio but distributes 1% in gains with 50% short-term, your tax cost is 0.30% for a 24% bracket investor. Another fund with 0.10% expense ratio and 0.1% distributions costs 0.13% total. The higher fee fund is cheaper after tax.

Step 5: If you hold multiple ETFs, consolidate to the most tax-efficient. For example, VOO (0.03%, low turnover) is better than SPY (0.0945%, higher turnover) in taxable accounts. The 0.0645% fee difference saves $64.50 per $100,000. The tax difference could save you hundreds.

Specific tools: use Morningstar's ETF Compare tool to see turnover and distribution history side by side. Use your broker's tax reporting to see past distributions. If you use IBKR, go to Reports > Tax > Cost Basis to see realized gains per holding.

If you must hold factor ETFs (e.g., low volatility, dividend growth), hold them in a tax-advantaged account like an IRA. Keep broad-market, low-turnover ETFs in taxable. This is the core strategy: match the ETF's tax profile to the account type.

Inversion: Do not use the same ETF across taxable and tax-advantaged accounts. A tax-inefficient ETF in a taxable account will cost you more in taxes than you save in fees. Check the fund's prospectus for "Principal Investment Strategies" to see if it uses derivatives or active trading. If it does, keep it in an IRA.

FAQ

How does ETF fee compression affect my investment returns?

Fee compression lowers the expense ratio, which increases your net return by the amount of the fee cut. For a 0.35% drop, you save $350 annually on a $100,000 portfolio. However, if the fund increases turnover to support that low fee, you may face higher capital gains distributions, which are taxable and can offset the fee savings. The net effect depends on your account type and the fund's distribution history.

What are the historical trends in ETF expense ratios?

The average U.S. equity ETF expense ratio fell from 0.50% in 2010 to 0.15% in 2023, a 70% decline. Vanguard launched the first low-cost index ETF in 2001, triggering the fee war. Today, broad-market ETFs like VOO charge 0.03%, while SPY charges 0.0945%. The trend is driven by competition and scale.

Are there any downsides to low ETF fees?

Yes, in taxable accounts. Low fees can lead to higher turnover or derivatives use to maintain profitability, triggering capital gains distributions. These distributions are taxable, and short-term gains are taxed at ordinary income rates up to 37%. A fund with a 0.10% fee but 2% in short-term gains distributions can cost more than a fund with a 0.20% fee and no distributions.

How do ETF fees compare to mutual funds?

Mutual funds typically have higher expense ratios, averaging 0.60% for index mutual funds vs. 0.15% for ETFs. Mutual funds also distribute gains more frequently due to daily cash flows, creating tax drag. ETFs are more tax-efficient due to in-kind creation/redemption, but fee compression can erode that advantage if it increases turnover.

What ETFs have the lowest expense ratios in 2024?

Vanguard's VOO (0.03%), iShares' IVV (0.03%), and Fidelity's FZROX (0.00%) are among the lowest. However, check turnover and distributions. FZROX has zero fees but is limited to Fidelity accounts and may have higher turnover. VOO and IVV have low turnover and minimal distributions, making them tax-efficient for taxable accounts.

Will ETF fee compression continue in the future?

Yes, but with limits. Fees cannot drop to zero because providers need revenue for operations and compliance. Inflation and regulatory costs may slow further cuts. However, competition will keep pushing fees down. The next battleground is tax efficiency and securities lending yield, not just expense ratios. Expect more funds to advertise "net cost after taxes" as a selling point.