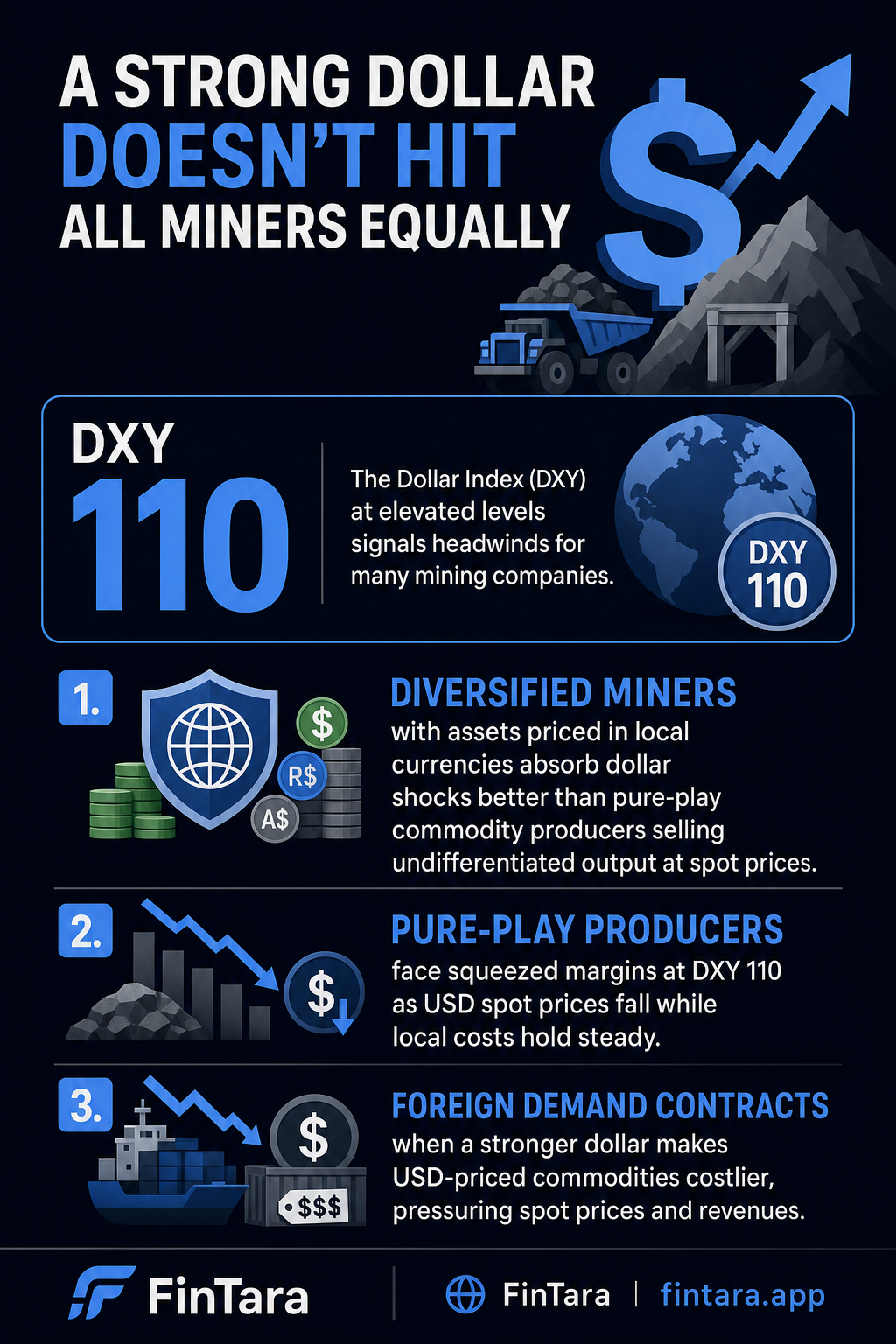

A DXY reading near 110 doesn't hurt all commodity stocks equally. Diversified miners with assets priced in local currencies absorb the dollar shock better than pure-play commodity producers selling undifferentiated output at spot prices. Choose diversified miners if you hold through multi-year cycles and want natural geographic hedges. Choose pure-play producers if you're positioned for a dollar reversal and want maximum leverage to commodity price recovery — accepting that DXY 110 will compress margins hard in the interim.

Quick Comparison: Diversified Miners vs. Pure-Play Producers

| Dimension | Diversified Miners | Pure-Play Commodity Producers |

|---|---|---|

| Dollar sensitivity | Moderate — revenue mix cushions spot exposure | High — near-total exposure to USD-denominated spot prices |

| Margin behavior at DXY 110 | Partially protected by non-USD cost bases | Squeezed from both sides: lower revenue, same costs |

| Geographic hedging | Built-in via multi-jurisdiction assets | Minimal unless hedging programs are active |

| Recovery upside | Lower — diversification caps the bounce | Higher — full beta to a dollar reversal |

| Volatility profile | Lower drawdowns in dollar-strength regimes | Steeper drops, steeper recoveries |

| Suited for | Cycle-agnostic long-term holders | Tactical traders positioned on DXY turning lower |

Why DXY 110 Bites Commodity Producers Harder Than the Headline Suggests

Local-currency assets cushion the dollar shock better than spot-price plays. — Photo by AlphaTradeZone on Pexels

Local-currency assets cushion the dollar shock better than spot-price plays. — Photo by AlphaTradeZone on Pexels

Commodity prices are denominated in U.S. dollars. When the dollar strengthens sharply, the same barrel of oil or tonne of copper buys fewer euros, reals, or Australian dollars. Foreign demand contracts at the margin. Spot prices fall. That's the standard explanation, and it's correct.

What the standard explanation skips: the cost structure doesn't move the same way.

A copper miner in Chile pays workers in pesos, services local contracts in pesos, and runs energy costs partially indexed to local rates. When DXY climbs to 110, those peso-denominated costs look cheaper in dollar terms — briefly. But the revenue drop hits immediately, and the cost benefit takes quarters to feed through. The interim period is where producers bleed.

Pure-play producers — a single-commodity, single-geography miner or driller — face this squeeze at full intensity. There's no other revenue stream to buffer it. Every dollar move in DXY shows up directly in their reported margins. When DXY sustains above 110, the market reprices their earnings estimates fast, and share prices follow.

This is the angle that generic DXY-vs-commodities coverage misses: it's not just a spot price problem. It's a timing mismatch between revenue compression and cost relief, concentrated most severely in single-commodity producers.

Where Diversified Miners Hold Ground — Geographic and Commodity Mix as a Natural Hedge

Diversified miners — companies with exposure across copper, gold, iron ore, and energy, spread across multiple continents — don't escape dollar strength. But their structure dilutes it.

Consider the mechanics. A miner with operations in Australia, Canada, and South America receives revenue in multiple currencies. When DXY rises, their USD-reported revenue from non-dollar-denominated sales contracts. But so do their costs, reported in the same local currencies. The hedge isn't perfect. It's partial. And partial is meaningful when pure-play producers have no hedge at all.

The commodity mix matters too. Gold has historically maintained a loose inverse correlation with the dollar, but it's not reliable across all dollar-strength regimes. Copper tracks global growth more than dollar direction in some cycles. A miner with exposure to both behaves differently than one selling only oil or only agricultural commodities, where USD pricing dominates nearly all transactions.

Diversified miners also carry lower drawdown risk in sustained dollar-strength regimes because institutional investors use them as long-cycle positioning vehicles. They don't get fully repriced on a single DXY spike the way a single-commodity producer does.

The trade-off is real, though. That same structural cushion caps the upside when the dollar reverses. A diversified miner at DXY 110 won't fall as far — but it also won't spring back as hard when DXY drops to 100.

Where Pure-Play Producers Win — Maximum Beta to a Dollar Reversal

Cover: Investor reviewing diversified miner stock performance with DXY chart overlay in modern office — Photo by Yan Krukau on Pexels

Cover: Investor reviewing diversified miner stock performance with DXY chart overlay in modern office — Photo by Yan Krukau on Pexels

Pure-play commodity producers are not a bad trade. They're a specific trade.

If DXY at 110 is near a cyclical peak — and dollar cycles do turn — then single-commodity producers offer the sharpest recovery profile. Their margins were the most compressed on the way up, so they expand fastest on the way down. Revenue recovers before costs re-inflate. The window of margin expansion can be brief but sharp.

This is why pure-play oil producers, copper miners, or agricultural commodity companies attract speculative positioning near perceived DXY peaks. The thesis isn't that dollar strength is good for them. It's that the market has already priced the damage, and the reversal will be asymmetric.

The problem is timing. No one knows when DXY 110 becomes DXY 108 or DXY 115. A trade that requires a specific macro reversal within a defined window is an explicit directional bet on the dollar — not a commodity equity thesis. Retail investors who buy pure-play producers at DXY 110 expecting a quick reversal are making a currency call, whether they've framed it that way or not.

foreign revenue losses dxy above 105That distinction changes the risk management entirely. A position requiring a macro catalyst has a different stop-loss logic than a position held on fundamental merit.

The Hidden Trade-Off: What Neither Side's Advocates Acknowledge

Advocates of diversified miners at DXY 110 rarely discuss the cost-structure illusion.

When dollar strength persists — not a spike, but a sustained regime above 110 for multiple quarters — local-currency cost advantages erode as regional inflation adjusts. Workers in Chile renegotiate. Energy contracts reset. Capital expenditure in local currency gets repriced. What looked like a cost cushion in quarter one looks much thinner by quarter three.

Pure-play producer advocates rarely discuss the balance sheet reality. High-dollar regimes typically accompany tighter global financial conditions. Producers carrying significant USD-denominated debt face a double pressure: margins compress as commodity prices fall, and refinancing becomes more expensive as rates stay elevated. A miner or driller that looked solvent at DXY 100 may face covenant stress at DXY 110 if the move is sustained and earnings revisions come through.

Neither of these dynamics is captured in the simple "strong dollar hurts commodities" frame. The actual damage mechanism for equities runs through earnings estimate revisions, balance sheet stress, and capital allocation decisions — not just spot price moves.

The market often reprices commodity producer equities faster than the actual earnings damage materializes. That creates a window where the stocks look oversold relative to current fundamentals — but current fundamentals haven't yet caught up to what DXY 110 implies for next quarter's margins.

Choose Diversified Miners If... / Choose Pure-Play Producers If...

Choose diversified miners if:

- You hold multi-year positions and don't want to time the dollar cycle

- Your commodity allocation is part of a broader equity portfolio, not a standalone macro trade

- You want reduced drawdown during sustained dollar-strength regimes, accepting lower recovery upside

- You're already exposed to single-commodity risk elsewhere in the portfolio and need natural diversification

Choose pure-play commodity producers if:

- You have a specific, time-bounded thesis on DXY reversal — and a defined exit if that thesis fails

- You're treating the position as a tactical trade, not a long-term holding

- You've assessed the balance sheet and confirmed manageable USD-denominated debt at current rates

- You're deliberately taking maximum dollar-reversal beta and understand the position may deepen before it recovers

Neither is inherently wrong. The error is holding a pure-play producer as if it were a long-term core holding during a sustained high-dollar regime — or dismissing pure-play producers entirely when DXY is signaling a potential peak.

As of Q2 2026, with the dollar index in an elevated range that has pressured commodity prices across multiple quarters, the distinction between these two buckets in a portfolio has become more consequential than most equity screeners capture. Screening for "commodity exposure" without distinguishing structure and geography misses the actual exposure you're running.

FAQ

Does DXY 110 automatically mean commodity stocks fall?

Not automatically — but the pressure is structural, not coincidental. Commodity prices are USD-denominated, so sustained DXY above 110 compresses revenues for producers selling into global markets. The degree of damage depends on each company's cost currency and debt structure. Diversified producers absorb more; single-commodity names take the full hit.

What makes a commodity producer "diversified" in this context?

Diversification here means two things: multiple commodities (copper plus gold plus energy, for example) and multiple operating geographies with costs in different local currencies. A miner operating only in one country but producing two metals is not fully diversified in the dollar-sensitivity sense that matters at DXY 110.

How does DXY 110 interact with commodity producer debt levels?

High-dollar regimes typically accompany elevated U.S. rates, which makes USD-denominated debt more expensive to refinance. A producer with heavy USD debt faces margin compression from falling commodity prices AND tighter refinancing conditions simultaneously. Balance sheet screening — specifically the currency breakdown of debt maturities — is essential before entering the sector at DXY 110.

Is gold a reliable hedge against DXY 110 pressure?

Gold has an inverse relationship with the dollar in many historical periods, but it's not consistent across all dollar-strength regimes. When dollar strength reflects a genuine global risk-off move, gold can hold up or rise even as DXY climbs. When DXY 110 reflects U.S. growth outperformance rather than crisis, gold may fall alongside other commodities. The driver of dollar strength matters more than the DXY level alone.

Should I use ETFs instead of individual commodity producer stocks at DXY 110?

A sector ETF covering miners or energy producers spreads the balance-sheet risk across holdings, which reduces single-stock blowup exposure. The trade-off: ETFs also dilute the recovery upside when DXY reverses. For investors without the time to screen individual producer balance sheets — especially USD debt maturities and hedge ratios — an ETF structure is the more appropriate vehicle during a sustained high-dollar regime.

Can commodity producers hedge out their DXY exposure?

Some do, through currency forwards and commodity price hedging programs. But retail investors rarely get clear visibility into the size and duration of those hedges in real time. A producer with active hedging looks resilient at DXY 110 on reported numbers — until the hedges roll off. Check the derivatives disclosure in quarterly filings, not just the margin line.

The trade-off isn't diversified vs. pure-play in the abstract. It's which dollar scenario you're actually positioned for — and whether your balance-sheet screening matches the macro regime you're sitting in.