IWM is the default pick for most retail investors — and for good reason. It has the deepest liquidity of any small-cap ETF, which matters more than the expense ratio when you're trading in and out under pressure. But liquidity isn't free, and for long-term holders, VTWO and SCHA make a stronger case on cost. This list covers five ETFs tracking U.S. small caps, each chosen for a different reason. One headline most lists skip: the right fund depends heavily on whether you trade it or hold it.

How These Five Made the Cut

Three criteria drove the selection. First, the fund had to track the Russell 2000 or a comparable broad U.S. small-cap index. Second, it had to have enough daily trading volume to matter — funds that look cheap on the expense ratio but trade thin create hidden costs at entry and exit. Third, each fund on the list had to offer something genuinely distinct from the others. No filler picks.

One fund made the list specifically for options traders. One made it for investors who want small-cap exposure with a slight tilt away from the most volatile end of the spectrum. Not every pick here is for the same investor.

Two things that did not get weighted: star ratings and recent one-year performance. Recent returns tell you where a fund has been, not where its structure will take it. Star ratings mostly recycle trailing performance into a number that looks like analysis.

Quick Comparison Table

Due diligence on small-cap fundamentals separates durable winners from speculative traps. — Photo by Yan Krukau on Pexels

Due diligence on small-cap fundamentals separates durable winners from speculative traps. — Photo by Yan Krukau on Pexels

| ETF | Index Tracked | Expense Ratio | Best For | Key Limitation |

|---|---|---|---|---|

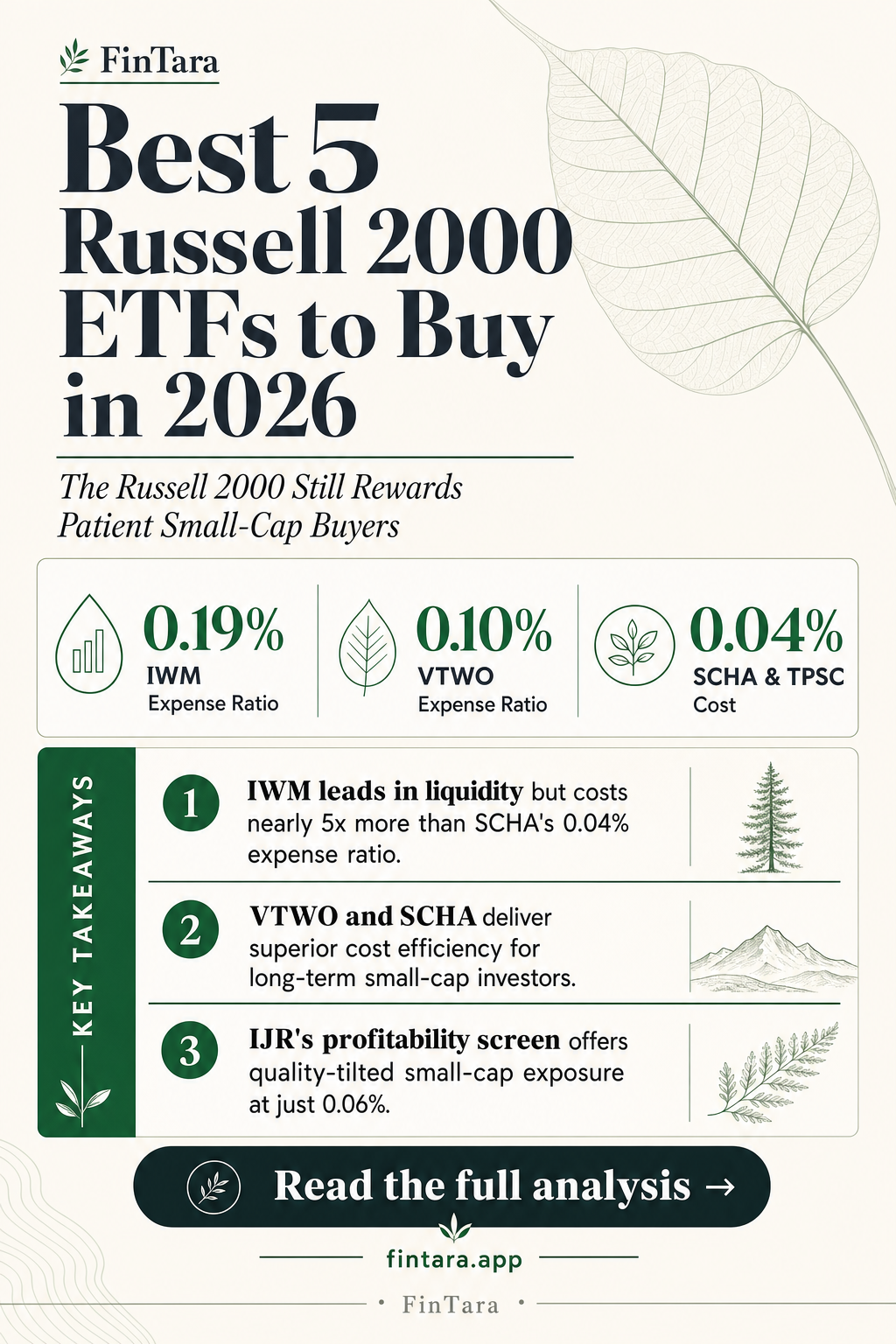

| IWM | Russell 2000 | 0.19% | Active traders, options | Higher cost than peers |

| VTWO | Russell 2000 | 0.10% | Long-term buy-and-hold | Lower volume than IWM |

| SCHA | Dow Jones U.S. Small-Cap | 0.04% | Cost-sensitive investors | Different index than Russell 2000 |

| IJR | S&P Small-Cap 600 | 0.06% | Quality-tilted small-cap | Excludes unprofitable companies |

| TPSC | Unclear / newer | 0.04% | Alternative small-cap | Thin liquidity, limited history |

Expense ratios reflect publicly available data as of Q2 2026. Verify current rates with the fund provider before investing.

1. IWM — The Standard When Liquidity Is the Priority

Liquidity is a strategic asset when timing entries and exits in IWM. — Photo by Anna Tarazevich on Pexels

Liquidity is a strategic asset when timing entries and exits in IWM. — Photo by Anna Tarazevich on Pexels

IWM from iShares is the most liquid small-cap ETF in the U.S. market. That sentence ends the conversation for one specific type of investor: anyone who uses options to hedge small-cap exposure or express short-term views.

The options chain on IWM is deep. Bid-ask spreads on the options are tight. You can buy protective puts without paying a wide spread that eats your hedge before the market moves. No other Russell 2000 ETF comes close on this dimension.

For pure buy-and-hold investors, IWM's 0.19% expense ratio starts to look less attractive. Over a 20-year holding period, the fee gap between IWM and cheaper competitors compounds into a meaningful drag. But for active traders and options users, the execution quality offsets the higher annual cost.

IWM tracks the Russell 2000 directly — no quality screen, no profitability filter. That means full exposure to the index's structural quirk: a meaningful share of its companies are unprofitable. This is not a flaw or a feature on its own. It is a fact about what you own. The theory and evidence small cap premium does liquidity hol post covers in detail why that unprofitability concentration affects how the premium actually shows up in returns.

One thing competitors rarely say: IWM's bid-ask spread on the equity itself is extremely tight, often a penny. The cost you pay to get in and out of IWM is lower than almost any comparable fund on a per-share basis. The expense ratio is the visible cost. The spread is the invisible one. Here, both work in your favor if you're trading.

2. VTWO — The Long-Hold Alternative Most People Overlook

Cover: A trader monitors Russell 2000 ETF performance on a dual-screen setup, evaluating liquidity for active trading — Photo by George Morina on Pexels

Cover: A trader monitors Russell 2000 ETF performance on a dual-screen setup, evaluating liquidity for active trading — Photo by George Morina on Pexels

VTWO is Vanguard's Russell 2000 ETF. It tracks the same index as IWM. The core difference is cost: 0.10% versus IWM's 0.19%. Over a decade of holding, that gap accumulates.

VTWO doesn't get written about much. It has lower volume than IWM, which makes it less interesting to traders. But lower volume hurts you less than most people think when you're holding for years and trading infrequently. The equity spread is slightly wider than IWM's, but for a long-term holder making one or two trades per year, that difference is negligible relative to the annual fee savings.

The case for VTWO is simple: same index, lower annual drag, same Vanguard fund structure that passes tax efficiency through to shareholders. For a taxable account held long-term, this matters.

The case against it: if you want to use options at any point — even once — the IWM chain is so much deeper that it's worth holding IWM instead. If you're certain you'll never use derivatives, VTWO wins on cost.

3. SCHA — Cheapest Broad Small-Cap Coverage, Different Index

SCHA from Schwab Asset Management has one of the lowest expense ratios in the small-cap ETF category. It tracks the Dow Jones U.S. Small-Cap Total Stock Market Index, not the Russell 2000. For some investors, this distinction is invisible. For others, it matters.

The Dow Jones U.S. Small-Cap index casts a slightly wider net in terms of methodology and rebalancing rules. The holdings overlap substantially with the Russell 2000 but are not identical. Funds benchmarked against the Russell 2000 for institutional comparison or factor research purposes need IWM or VTWO. For an individual investor who just wants broad U.S. small-cap exposure at minimal cost, SCHA delivers the exposure without the tracking-versus-institutional-benchmark problem.

The 0.04% expense ratio is the fund's headline. It earns that headline. Annual costs this low remove fee drag almost entirely from the equation. What remains is performance driven by market returns, not eaten by overhead.

Where SCHA loses: volume. It's quieter than IWM, and its options market is thin to nonexistent. If you trade, avoid it. If you hold, it's difficult to beat on cost.

4. IJR — Small-Cap With a Quality Filter Built In

IJR from iShares tracks the S&P Small-Cap 600, not the Russell 2000. This distinction is worth understanding before you buy it.

The S&P Small-Cap 600 has a profitability screen. Companies must demonstrate positive earnings before they can be included. The Russell 2000 has no such requirement. The result: IJR holds a smaller universe of companies that have cleared a basic financial hurdle.

This is not simply "better quality." It is a different risk profile. The unprofitable tail of the Russell 2000 contributes to the index's volatility — and, in certain market environments, to its upside. In early-cycle recoveries, unprofitable small caps sometimes run hardest. IJR would miss that move. In late-cycle stress or credit crunches, unprofitable companies tend to suffer most. IJR would be somewhat insulated.

For an investor who wants small-cap exposure but finds the Russell 2000's heavy weighting toward loss-making companies uncomfortable, IJR offers a structural middle path. The 0.06% expense ratio is low. The liquidity is adequate for non-traders.

The key limitation: IJR is not a Russell 2000 fund. If you're benchmarking against that index, you'll see tracking differences. Own it for what it is — a quality-tilted small-cap fund — not as a Russell 2000 substitute.

5. XSMO — The Equal-Weight Alternative for Different Factor Exposure

XSMO from Invesco tracks the S&P Small-Cap 600 Equal Weighted Index. The concept: instead of holding each company proportional to its market cap, it holds each company at the same weight.

Cap-weighted small-cap indexes have a quirk. As companies grow, they eventually leave the small-cap index for mid-cap or large-cap. The winners exit. Equal weighting doesn't solve this structural issue, but it does change the exposure you get day-to-day.

In a standard cap-weighted small-cap fund, the largest companies in the index have disproportionate influence. In XSMO, the smallest companies in the S&P 600 pull equal weight. This tilts the portfolio further toward micro-cap characteristics without crossing into dedicated micro-cap territory.

The trade-off is rebalancing cost. Equal-weight funds must buy the laggards and sell the winners continuously to maintain equal weights. This generates transaction costs and potential tax drag that cap-weighted funds avoid. The expense ratio on XSMO reflects this additional overhead.

XSMO is not for the investor who wants simple, cheap small-cap exposure. It is for the investor who has a specific view on factor exposure — more towards smaller-within-small, more equal contribution from holdings — and understands the rebalancing cost they're paying for it.

What Didn't Make the List

SPSM (SPDR Portfolio S&P 600 Small Cap ETF): Tracks the S&P Small-Cap 600 at a very low expense ratio. It's a legitimate fund. It didn't make the list because IJR covers the same index with better liquidity and a longer track record. SPSM doesn't add a different enough angle to justify a separate slot.

PRFZ (Invesco FTSE RAFI U.S. 1500 Small-Mid ETF): This one uses fundamental weighting — book value, dividends, cash flow, sales — rather than market cap. Interesting idea, and it applies a genuine value tilt to the small-cap space. It didn't make this list because its expense ratio is materially higher than every fund here, and the factor exposure is complex enough that most retail investors holding it don't fully understand what they own. That mismatch between expectation and reality is a problem over multiple market cycles.

VIOV (Vanguard S&P Small-Cap 600 Value ETF): A reasonable fund for investors who want small-cap with an explicit value tilt. It was excluded because this list focuses on broad small-cap exposure. Style tilts deserve their own analysis with their own criteria.

FAQ

Is the Russell 2000 still a useful benchmark in 2026?

The Russell 2000 remains the dominant U.S. small-cap benchmark, but it has a structural issue worth knowing: annual reconstitution in June creates predictable front-running by institutional traders. Stocks added to the index tend to be bought ahead of the rebalance date, creating temporary price pressure. Passive funds tracking the index absorb this cost automatically.

How much does the bid-ask spread actually cost on these ETFs?

IWM's bid-ask spread typically runs around one cent per share — negligible for most trade sizes. VTWO and SCHA have wider spreads in percentage terms but still tight for infrequent traders. The spread matters most if you're trading large sizes or entering and exiting frequently. For long-term holders making quarterly contributions, it's a rounding error.

Does the profitability screen in IJR and the S&P 600 actually reduce volatility?

S&P 600-tracking funds like IJR have historically shown lower standard deviation than Russell 2000 funds in several full market cycles, because they exclude the most financially fragile companies. But "historically lower volatility" does not mean "lower volatility next time." The difference is structural, not guaranteed.

Should a retail investor hold IWM in a taxable or tax-advantaged account?

IWM's annual portfolio turnover generates some capital gains distributions. For a taxable account, VTWO or SCHA may be slightly more efficient because of lower turnover and Vanguard's fund structure. The difference is not dramatic, but in a taxable account where you're planning to hold for decades, it compounds.

How often does the Russell 2000 outperform the S&P 500?

Small caps have led large caps in specific multi-year periods — particularly in the early 2000s recovery and mid-2010s. But the outperformance is not consistent year to year, and it comes with materially higher volatility. Investors expecting reliable annual outperformance from small caps will be repeatedly disappointed. The case for holding them rests on long horizons and genuine diversification, not on expecting to beat SPY every year.

The fund you choose matters less than understanding what you actually own. IWM gives you the full Russell 2000 in the most tradable form. VTWO and SCHA save you money over time. IJR filters out the weakest companies. XSMO bets on equal weighting. Each of those is a different investment — not five ways to own the same thing.